Buy and Borrow

How to Refinance an Auto Loan (Video)

August 11, 2020

If you are hoping to lower your interest rate or reduce your monthly payments, you may want to refinance your car loan. There are a number of reasons to refinance an auto loan, but do you know what steps are needed once you make the decision?

Here are the steps to take if you’re ready to refinance your car.

- The loan’s interest rate and monthly payment

- The remaining balance on the loan

- The loan term (how many months left to repay the loan)

- Your car’s vehicle identification number (VIN)

- Your driver’s license and Social Security number

- Current pay stubs or other proof of employment or income

1. Assess Your Credit

It’s always a good idea to monitor your credit, especially when you know you are going to apply for a loan. If you want to apply for an auto refinance to get a better rate, it’s smart to have an idea of your credit score before applying.

If you have been making payments on time and haven’t had other credit issues, your credit score may have improved since you first applied for your auto loan. That is a good sign, as an improved score could help you get a better rate.

If your credit score has decreased, this does not mean you cannot refinance your loan. Just keep in mind that your credit score will influence if you get approved and what the new interest rate will be.

2. Gather Needed Documents and Information

Before applying for a car refinance, take a moment to gather all of the material you’ll need. For your current auto loan, you’ll need to know:

You should also verify that your current loan does not have prepayment penalties. Having a copy of your loan contract will make this process easier. If you don’t have the original contract, reach out to your lender for a copy.

Other items you will need to complete your refinance application may include:

3. Apply and Decide

Once you have your materials gathered, you’re ready to apply for an auto refinance. When your application is approved, you can also decide if you want to keep your current length of your loan or adjust it.

If your goal is to save money over time, you might want to pay the loan off faster. This will help you pay less interest during the life of your loan.

If your goal is lower your payments to give your budget a boost each month, you could extend the term of your loan to help provide some cushion. This could be a good option if you are struggling to keep up with higher monthly payments, as it can help you continue to pay bills on time so your credit score won’t take a hit.

4. Finalize the Refinance

After you are approved for a refinance and you’re ready to accept, you can begin finalizing the refinance process. The lender will provide new loan documents for you to sign that details your new interest rate and term length.

The financial institution for the new loan then pays off the original loan. You now have a brand new loan with the new lender and can begin making payments to them at your new rate.

Ready to Refinance? If you want to lower your interest rates or monthly car payments, we’re here to help.

Category

Buy and Borrow

Tags

Buy and Borrow

What’s Needed for a Business Loan?

Before you apply for a business loan, learn about the eligibility requirements and what is needed to qualify for a small business loan.

Simply Suncoast

Credit Union Near Me… No Matter Where I Am

When you are looking for a credit union nearby, there is something wonderful you should know. Even if your credit union is not in the area, you can likely access credit union services.

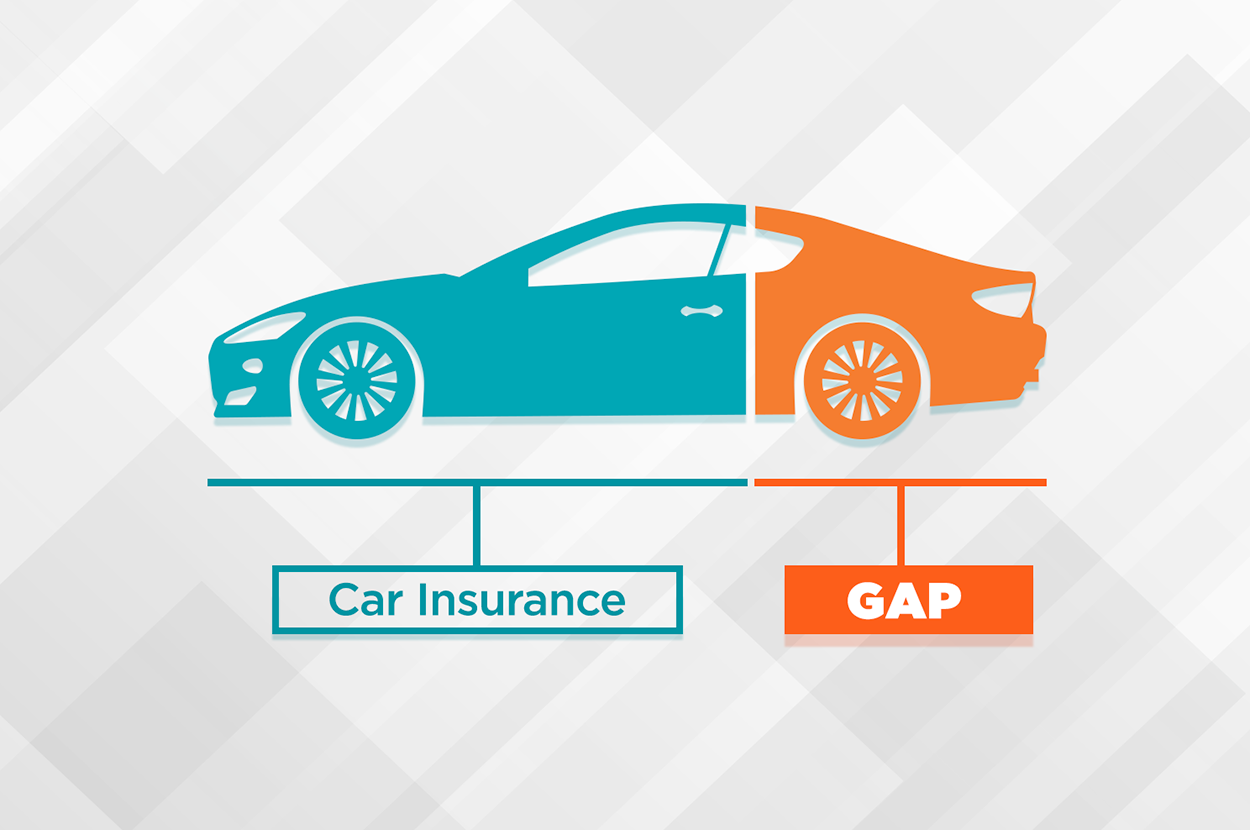

Safety and Protection

What Is GAP and What Does it Cover?

If you’re making car payments, Guaranteed Asset Protection (GAP) is a type of coverage that can save you a ton of money if your car is lost or totaled. Let’s explore what GAP is and what it covers.

Find a Branch or ATM

We’re local, serving multiple counties in Florida