Plan and Retire

What You Need to Know About the CARES Act

April 13, 2020

The Coronavirus Aid, Relief, and Economic Security (CARES) Act was created to help Americans impacted by COVID-19. Since the CARES Act will provide $2 trillion in relief, it has implications for many people.

Here is what you should know about the CARES Act:

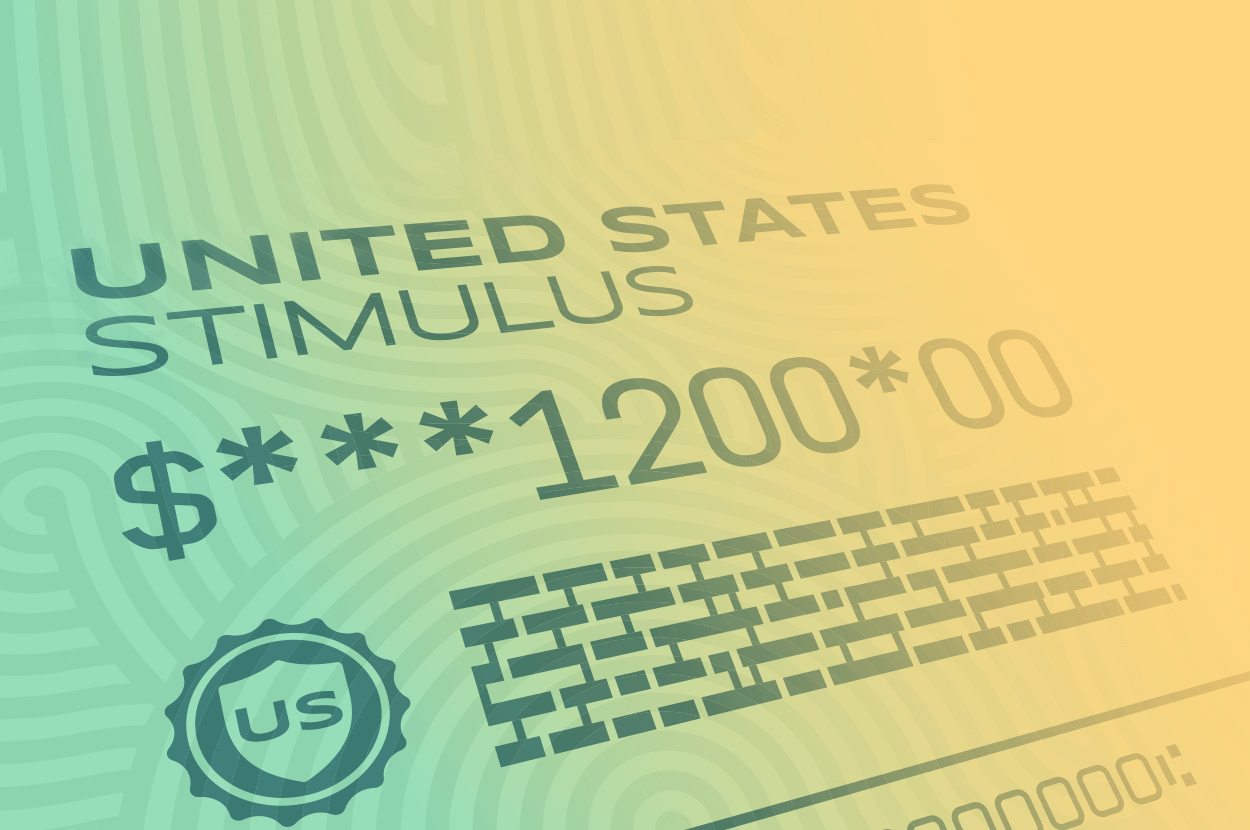

Stimulus Check Information

Part of the CARES Act provides Americans with a one-time payment of up to $1,200 for individuals or $2,400 for married couples. There is also an additional $500 per child under 17 years old.

If you have already filed your 2019 tax returns, your payment will be based on your 2019 information. If you haven’t filed your 2019 taxes yet, your payment will be based on your 2018 information.

Your stimulus check amount is based on your annual earnings. Individuals who made more than $75,000 or couples who made more than $150,000 will receive a reduced payment. People who made more than $99,000 as an individual (or $198,000 as a couple) will not receive a stimulus check.

Most people will not need to take action to receive their payment. You can find the latest information and answers to your frequently asked questions about stimulus payments by visiting the IRS website.

Business Owner Relief

The CARE Act also allocates $500 billion to help businesses with things like loans, loan guarantees or investments. From the Paycheck Protection Program to help cover the cost of retaining employees to Economic Injury Disaster Loans, there are a number of resources available to help businesses through this trying time.

Check out The Small Business Owner’s Guide to the CARES Act for more information about business owner relief.

Some Distributions can be Waived and Minimum Required Distributions are Suspended

The CARES Act gives people with inherited 401(k)s or Individual Retirement Accounts (IRAs) the option to suspend distributions in 2020. Required distributions don't apply to individuals with Roth IRAs, however, they do apply to investors with inherited Roth accounts.

Minimum required distributions that people usually must take from their 401(k)s and IRAs are also suspended for 2020.

Waived Withdrawal Penalties

Retirement plans and IRAs typically have withdrawal penalties for people who take out money before age 59½. However, the CARES Act temporarily waives the 10% early withdrawal penalty for 2020 and allows the account holder to withdraw up to $100,000 from their retirement plan or IRA without incurring the penalty. However, you will still owe the tax on these funds.

Help Is Here If You Need It

COVID-19 has brought unprecedented new challenges to our communities, but help is available.

For information about Coronavirus Tax Relief and Economic Impact Payments, visit the irs.gov/coronavirus.

For information about how Suncoast is helping members, visit our emergency page.

For information about whether these special 2020 distribution rules are appropriate for your situation, please contact Suncoast Investment Services at 866.300.9382 or invest@suncoastcreditunion.com.

This information has been derived from sources believed to be accurate. Please note - investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

Under the CARES act, an accountholder who already took a 2020 distribution has up to 60 days to return the distribution without owing taxes on it. This material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. Under the SECURE Act, in most circumstances, once you reach age 72, you must begin taking required minimum distributions from a Traditional Individual Retirement Account (IRA). Withdrawals from Traditional IRAs are taxed as ordinary income, and if taken before age 59½, may be subject to a 10% federal income tax penalty. You may continue to contribute to a Traditional IRA past age 70½ under the SECURE Act, as long as you meet the earned-income requirement.

Accountholders can always withdraw more. But if they take less than the minimum required, they could be subject to a 50% penalty on the amount they should have withdrawn – except for 2020.

Citations:

1 - CNBC.com, March 25, 2020.

2 - The Wall Street Journal, March 25, 2020.

3 - The Wall Street Journal, March 25, 2020.

4 - The Wall Street Journal, March 25, 2020.

Suncoast Investment Services is a marketing name used by Suncoast Credit Union. Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. Suncoast Credit Union and Suncoast Investment Services are not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Suncoast Investment Services, and may also be employees of Suncoast Credit Union. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of, Suncoast Credit Union or Suncoast Investment Services. Securities and insurance offered through LPL or its affiliates are:

| Not Insured by NCUA or Any Other Government Agency | Not Credit Union Guaranteed | Not Credit Union Deposits or Obligations | May Lose Value |

Category

Plan and Retire

Tags

Buy and Borrow

What’s Needed for a Business Loan?

Before you apply for a business loan, learn about the eligibility requirements and what is needed to qualify for a small business loan.

Simply Suncoast

Credit Union Near Me… No Matter Where I Am

When you are looking for a credit union nearby, there is something wonderful you should know. Even if your credit union is not in the area, you can likely access credit union services.

Safety and Protection

What Is GAP and What Does it Cover?

If you’re making car payments, Guaranteed Asset Protection (GAP) is a type of coverage that can save you a ton of money if your car is lost or totaled. Let’s explore what GAP is and what it covers.

Find a Branch or ATM

We’re local, serving multiple counties in Florida